Go Lean Commentary

“Give me my money!”

This is not so unfamiliar a phrase in pop culture. It refers to the everyday scenario of repaying a debt. People want to be re-paid what is owed them. Many times, the motivation for street crimes is the defaulting of a debt – legitimate or illicit. Even more so, countries have gone to war over debt defaults; consider the experience of the Mexican – French Drama, better known as “Cinco De Mayo”. (The book Go Lean … Caribbean also relates the bad experiences of the Egyptian Default in the 1870’s – Page 143).

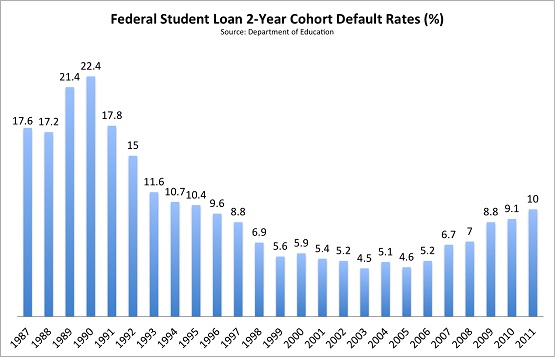

There are standards of quality that we all accept when it comes to debt collection; it is like a yardstick of success. That figure is 10 percent. Any lending institution with a default rate higher than 10% is automatically considered a failure. Many times, the institution – like banks – would come under external supervision for sporting such a default rate.

For the American student loans eco-system, the default rate has remained consistently below 10 percent, (now after the implementation of collections best practices in the 1990’s), even during dire economic conditions. Though there have been complaints of upward creeping, that argument is all relative; see chart here:

According to the following news article, the Caribbean experience is “bad” for gleaning returns from their student loans, even as a straight banking product: principal & interest dynamics. How bad? 10 percent? That would be a dream; the experience in one country, the Bahamas is 75 percent for student loans. See the news article to this effect here:

Title: Bahamas government warns student loan defaulters of legal action

Posted: March 1, 2016; retrieved July 8, 2016 from http://www.caribbean360.com/news/bahamas-government-warns-student-loan-defaulters-of-legal-action

NASSAU, The Bahamas – Minister of Education, Science and Technology Jerome Fitzgerald has put recipients of the Education Loan Programme (ELP) on notice that if they fail to repay their loans they will face court action.

Despite the many “success” stories coming out of the ELP, he maintained that there were also a number of failings which have “derailed” the programme.

Since passage of the Act in 2002, a total of 4,733 people have benefited from the programme. But the initiative was suspended in August 2009 because of a 75 per cent delinquency rate in loan repayments.

“This was and is clearly unsustainable. The people of the Bahamas financed this programme to assist with the education of persons pursuing tertiary education. The loan portfolio is intended to be a revolving fund; and as the borrower pays, the monies are repaid to assist other qualified students,” Fitzgerald said at a press conference yesterday.

“I must emphasize that many loan recipients have satisfied and are satisfying their commitments. There are many more, however, for a plurality of reasons, who have not. We are aware that many persons who received loans have returned home and are not working. We are also equally aware that there is a possibility that a number of persons who received funds between 2000 and 2002 may not have ever attended school. However, we are cognizant of our fiduciary responsibility to the country and that we had to formulate a plan that would sensibly facilitate our pursuit to collect delinquent funds, one way or the other.”

Fitzgerald explained that, with a view of jumpstarting the programme, the ELA was mandated to review the suspended it with the intention of making recommendations to restarting to give an opportunity to qualified persons interested in pursuing tertiary education.

He said that after three years of reviewing and reconciling records, the Education Loan Authority now has a formula to address and correct the deficiencies of the ELP.

“I can assure that the Directors and Management of the Education Loan Authority (ELA) were instructed to work fastidiously, to come up with a solution to . . . not only restore the programme, but to restore the programme with the necessary control provisions to ensure its ongoing sustainability and viability,” the minister said.

Fitzgerald re-emphasized government’s position that “one of the prerequisites for successfully delivering our commitment to the creation of an effective transition path from high school into higher education had to be the restoration of the Scholarship Loan Programme.”

On October 21, 2015 the Education Loan (Amendment) Act 2015 came into force. In addition to collecting funds, the new Act addresses delinquencies, rewards borrowers who are paying and/or genuinely want to honour their obligations, and empowers the ELA to collect funds.

In summary, the Bahamas Education Loan Authority (ELA) is owed over $155 million in outstanding loan payments for its student loan scheme, with a default rate of 75 percent.

This Caribbean community should now be saying: “Give me my money!”

However, this commentary extends the criticism further: The money being demanded is the principal and maybe even some interest amounts due. But student loans are supposed to be investments in the young people of the community. This commentary trumpets the reality of Caribbean student loans as a fallacy: Where is the return on these investments?

This commentary asserts that those who advocate to remediate Caribbean economics needs to avoid a series of Economic Fallacies. This is commentary 3 of 6 from the movement behind the Go Lean book on the subject of Economic Fallacies. As related in the first submission on this series, the situation in the Caribbean region is likened to the imagery of an animal foraging for food, but then gets distracted and “chases a squirrel up a tree”. The squirrel in the tree will never be a meal; it is just a waste of time and energy for the animal. This analogy conveys the waste of time associated with a frivolous and fallacious pursuit. The other commentaries detailed in this series are as follows:

- Independence – Hype of Hope

- Austerity – Book Review: Mark Blyth’s “History of a Dangerous Idea”

- Education & Student Loans – Not a good Return on Investment

- Phillips Curve – Fallacy of Minimum Wage

- Self-regulation of the Centers of Economic Activity

- Casino Currency – US Dollars?

All of the commentaries in this series are economic in nature. They refer to rules for managing the valuable resources of time, talents and treasuries. Student loan investments are extending all three of these resources. Despite the direct reference to this one Caribbean member-states – the Bahamas – the experience is similar through out the entire region: Student loans have been a bad investment; lose-lose for the community. A mission of the roadmap gleaned from the Go Lean book, is to remediate the economic chaos in the region.

Back to the Bahamas, in addition to a terrible loan default rate where they report only 16 percent of borrowers are up to date on their loan payments; the problem is exacerbated by an atrocious brain drain rate. Some studies present that 70 percent of college educated ones in the Caribbean in general have fled the region for residency abroad. (The Bahamas rate was 61 percent in that report). Surely investments in student loans as a nation-building policy is an economic fallacy … for the Bahamas in particular and the Caribbean region in general.

The problem is not just a Caribbean one. Other communities also experience dysfunction in their student loan eco-system. For example, in the US, the average student loan debt for recent college graduates is close to $30,000; any loans guaranteed by the US Federal government is non-dischargeable, so even after death or bankruptcy, the indebtedness remains. This type of debt impedes the individual from making methodical progress, and the experience on community economics have been imperiled. In a previous blog-commentary, it was reported how the student loan crisis has impacted the home-buying practice.

So the best practice for students, who have partaken in a loan program, is to strategize a repayment; see related article in the Appendix. There are economic consequences for the individual and the community.

Education is good!

Student loans are bad!

The entire college education eco-system has had mixed results for the Caribbean.

Part of the Caribbean’s dismal record with college education is tied to the reality of college graduates abandoning the homeland, or never returning after their matriculation. This consideration aligns with the book Go Lean…Caribbean, a roadmap to elevate the economic, security and governing engines of the Caribbean. The Caribbean wants to model many of the good examples of the United States, and learn from the many bad cautionary tales. Education is a good model; (every additional year of schooling – in the aggregate – raises a community’s economic output by 3% to 6%). On the other hand, the eco-system for student loans is one bad American model we do not want to emulate. The Go Lean book detailed the new debt crisis America is contending with because of the excessive debt loads, young ones are being burden with (Page 114). Here is an excerpt:

The Bottom line on a New Student Loan Scandal

Matt Taibbi, the Rolling Stone magazine contributing editor, had previously exposed the 2008 Wall Street Crisis in his critically acclaimed book Too Big To Fail. Now he exposes as scandalous how American colleges exploit young students with outrageous tuition increases (3 X the inflation rate), since all are approved for federal student loans. Where there is demand, a supply system steps in to deliver … and profit. But this industry creates its own demand with slick marketing campaigns. See Appendix IH of Go Lean … Caribbean – Page 286.

Already too, the Caribbean has its own bad experiences within its own student loan eco-system. The Caribbean experience has been more negative than positive. Too many of our students have left … to study abroad; then refused to return home, taking with them the return on community investments and repayment of their student loans. We must do better! A Go Lean/CU mission is to dissuade our citizens from emigrating to foreign shores.

This Go Lean book serves as a roadmap for the introduction and implementation of the technocratic Caribbean Union Trade Federation (CU). The CU has a complete education agenda, applying lessons learned from the consideration of other communities, like the US. This roadmap presents the following 3 prime directives:

- Optimization of the economic engines in order to grow the regional economy to $800 Billion & create 2.2 million new jobs..

- Establishment of a security apparatus to protect the resultant economic engines.

- Improvement of Caribbean governance to support these engines.

Again, education is good. So the Go Lean roadmap provides turn-by-turn directions on how to reform the Caribbean tertiary education systems, economy, governance and Caribbean society as a whole. There is a plan for a regional student loan pool, where we mitigate the dangers that are so evident in the American eco-system.

As for the primary threat of constant societal abandonment – of crisis proportions – the Go Lean roadmap has missions to remediate this crisis. So as a planning tool, the roadmap commences with a Declaration of Interdependence, pronouncing the dread of threats and Caribbean brain drain (Page 12):

xvi. Whereas security of our homeland is inextricably linked to prosperity of the homeland, the economic and security interest of the region needs to be aligned under the same governance. Since economic crimes … can imperil the functioning of the wheels of commerce for all the citizenry, the accedence of this Federation must equip the security apparatus with the tools and techniques for predictive and proactive interdictions.

xix. Whereas our legacy in recent times is one of societal abandonment, it is imperative that incentives and encouragement be put in place to first dissuade the human flight, and then entice and welcome the return of our Diaspora back to our shores …

xxi. Whereas the preparation of our labor force can foster opportunities and dictate economic progress for current and future generations, the Federation must ensure that educational and job training opportunities are fully optimized for all residents of all member-states, with no partiality towards any gender or ethnic group… This responsibility should be executed without incurring the risks of further human flight, as has been the past history.

So a tertiary education plan, without addressing the preponderance of brain drain is another economic fallacy. We, as a community, would be spending good money, but getting bad returns.

Make no mistake, the Go Lean movement (book and accompanying blog-commentaries) posits that education is a vital consideration for Caribbean economic empowerment. Imagine better regional institutions with conditional loans with cross-border enforcement and collections. The vision of the CU is a confederation of the 30 member-states of the Caribbean to do this type of heavy-lifting to champion better educational policies for our region.

The book details the policies; the community ethos to adopt, plus the executions of the following strategies, tactics, implementations and advocacies to impact the tertiary education in the region:

| Community Ethos – Deferred Gratification | Page 21 |

| Community Ethos – Economic Systems Influence Choice | Page 21 |

| Community Ethos – Job Multiplier | Page 22 |

| Community Ethos – Lean Operations | Page 24 |

| Community Ethos – Return on Investments (ROI) | Page 24 |

| Community Ethos – Ways to Impact the Future | Page 26 |

| Community Ethos – Ways to Foster Genius | Page 27 |

| Community Ethos – Ways to Help Entrepreneurship – Training & Mentoring | Page 28 |

| Community Ethos – Ways to Impact Research and Development – STEM Education | Page 30 |

| Strategy – Competition Analysis – Study: At home –vs- Abroad | Page 50 |

| Tactical – Separation of Powers – Education Department | Page 85 |

| Tactical – Separation of Powers – Labor Department – On-the-Job-Training Regulator | Page 89 |

| Implementation – Ways to Better Manage Debt | Page 114 |

| Planning – Lessons Learned from Egypt | Page 151 |

| Advocacy – Ways to Grow the Economy | Page 151 |

| Advocacy – Ways to Create Jobs | Page 152 |

| Advocacy – Ways to Improve Education | Page 159 |

| Advocacy – Ways to Impact Student Loans – How to Reboot | Page 160 |

| Advocacy – Ways to Improve Governance | Page 169 |

| Appendix – Education and Economic Growth | Page 258 |

| Appendix – New American Student Loan Debt Crisis – Now Over $ 1 Trillion in Debt | Page 286 |

The American Tertiary Education Student Loan eco-system is a broken model. This constitutes a fallacy for the Caribbean to emulate it. This point, and other fallacies related to education, have been repeatedly addressed and further elaborated upon by this Go Lean movement, as in these previous blog/commentaries:

| https://goleancaribbean.com/blog/?p=7806 | Skipping School to become Tech Giants |

| https://goleancaribbean.com/blog/?p=6269 | Education & Economics: Welcome Mr. President |

| https://goleancaribbean.com/blog/?p=5482 | For-Profit Education: Plenty of Profit; Little Education |

| https://goleancaribbean.com/blog/?p=4487 | FAMU – Finally, A Model for Facilitating Economic Opportunity |

| https://goleancaribbean.com/blog/?p=1470 | College of the Bahamas Deficient Master Plan for 2025 |

| https://goleancaribbean.com/blog/?p=1256 | Is a Traditional 4-year Degree a Terrible Investment? |

Let’s do better here in the Caribbean. Better than our American model – see the VIDEO in the Appendix – and better than our own status quo. Let’s own up to the hurtful fact that tertiary education – and the student loans to finance them – has been an economic fallacy! We have been chasing “the squirrel up the tree and then waiting with futility for it to come down”. The Caribbean expression is so apropos here:

Fattening frog for snake.

There is a better way!

The people, educational and governing institutions in the region are urged to lean-in for the empowerments described in the book Go Lean … Caribbean. Education reform – weeding out the fallacies – can succeed in elevating Caribbean society; we can make the homeland better places to live, work, learn and play. 🙂

Download the book Go Lean … Caribbean – now!

================

Appendix VIDEO – 5 Reasons Student Loans are Bulls**t | Decoded | MTV News – https://youtu.be/q0j0xnwEQug

Published on Oct 28, 2015 – Student Loans! Whether you hate them or hate them, you’re probably going to have to deal with them in one way or another. Why? Because over 40 Million young(ish) Americans owe over 1.2 Trillion dollars in student loan debt and millions of others have this spectre of debt loom over crucial life decisions. And while there are no easy answers about what to do about it, there are a lot of good questions like: Why has tuition across the United States skyrocketed over the past 30 years? What are your student loans really paying for? Is there anything you can do? And perhaps most importantly, is this all just a bunch of Bullshit?

Franchesca Ramsey: https://twitter.com/chescaleigh

Brought to you with love by: http://mtvother.com

Produced by: http://www.kornhaberbrown.com

With Special Guest:

Ben O’Keefe (@benjaminokeefe)

Watch Ben’s Show: The O’Keefe Brief

http://front.moveon.org/tag/the-okeef…

To learn more, visit: http://studentdebtcrisis.org/

—————————–

Appendix – Tips for repaying student loans

By: Andrew Housser

Source: Retrieved July 8, 2016 from: http://www.newson6.com/story/25551775/tips-for-repaying-student-loans

The average student loan debt for recent college graduates is close to $30,000. During the first five years after college, four out of 10 borrowers become delinquent in repaying their student loans. This can lead to extra fees and interest costs, as well as a major hit to one’s credit rating. If you are a college graduate who is struggling to keep up with payments, these tips can help.

The average student loan debt for recent college graduates is close to $30,000. During the first five years after college, four out of 10 borrowers become delinquent in repaying their student loans. This can lead to extra fees and interest costs, as well as a major hit to one’s credit rating. If you are a college graduate who is struggling to keep up with payments, these tips can help.

Understand the terms of your loan(s). Chances are, you have more than one loan with different lenders. As a result, your options for loan repayment will vary. The U.S. Department of Education’s National Student Loan Data Systemprovides loan amounts, lender information and repayment status for all government-funded federal student loans. Private student loans are financed through a bank, credit union or other nongovernmental lender. Private lenders set their own interest rates, loan limits and other conditions. You will need to contact your private lender directly to obtain full details on the terms of your loan.

Consider consolidation. It is challenging to keep track of multiple loan payments. Consolidating your student loans will create a more convenient single monthly payment. Consolidation does increase the term of the loan and the amount of interest paid over the life of the loan. However, by extending the repayment term, it can reduce your monthly payments by almost half.

Figure out your repayment plan. Some loans have a grace period of six to nine months before the first payment is due. Depending on the loan type, interest may or may not accrue during this period. Having a little bit of breathing room after graduation can be helpful as you find and start a job. However, it also makes it easy to forget that a payment is due. Up to a third of borrowers miss their first student loan payment. Your credit rating can take a hit with just one missed payment. Automatic payments set up through your bank checking account can ensure you meet your financial obligation each month. Some lenders offer discounts for these automatic debits, too.

Do not default. Should you find yourself unable to make loan payments due to a job loss or other circumstances, it is always better to work with your lender to find a repayment solution than to default. Penalties for defaulting on student loans can be severe. They can include garnished wages and Social Security benefits, and government retention of tax refunds. In addition, you may incur late fees and collection charges. Instead of defaulting, consider these other options:

Deferment. If you qualify, you can temporarily halt payments on the loan principal by applying for a loan deferment with your lender. During this time, the federal government will pay the interest on subsidized federal student loans, but not unsubsidized loans.

Forbearance. A forbearance allows you to temporarily modify your loan terms by stopping or reducing monthly payments, or extending the repayment time period. Depending on your situation, you may or may not have to pay interest on the loan during a period of forbearance.

Forgiveness. Loan forgiveness programs eliminate loan balances (and payments) for people who meet certain criteria. These include working in eligible public service positions, such as in law enforcement or public health; military service; volunteer work; and teaching or practicing medicine in a low-income, rural area.

Cancellation. In extreme cases, such as disability, you may be able to get your loans discharged.

If you are still in school, make sure you complete an exit counseling session with a financial aid officer at your school before your graduate. This representative will review the terms and conditions of your loans, including repayment options and your rights and responsibilities. This is the time to ask questions and map out a plan for repayment. Then you can focus on the really important tasks like landing that dream job and starting your bright future.

About the Author

Andrew Housser is a co-founder and CEO of Bills.com, a free one-stop online portal where consumers can educate themselves about personal finance issues and compare financial products and services. He also is co-CEO of Freedom Financial Network, LLC providing comprehensive consumer credit advocacy and debt relief services. Housser holds a Master of Business Administration degree from Stanford University and Bachelor of Arts degree from Dartmouth College.