Go Lean Commentary

Income Inequality = the rich becoming richer while the middle classes shrink.

A phrase like Income Inequality, on the surface, would appear to be just about economics. But truthfully this is more a subject about governance, but yes, in alignment with economic and security concerns.

The book Go Lean…Caribbean and accompanying blogs constantly focus on economics, security and governance in the Caribbean region. The book serves as a roadmap for the introduction and implementation of the technocratic Caribbean Union Trade Federation (CU). If this effort is successful then it could result in some abatement of Income Inequality.

The subject of Income Inequality has been influx more and more as of late, especially after the Great Recession of 2008 – a frequent topic for the Go Lean book and accompanying blogs. The desire to eliminate or reduce Income Inequality is a practical argument for social cohesion and to reduce social unrest; as such eruptions can weaken society. Income Inequality has a slippery slope that can lead to down to Failed-State status. Now after waging global conflicts of World War I, World War II plus countless regional conflicts and sectarian violence, it is important for societies to be “on guard” for encroachments in this regard.

Thusly, Income Inequality is a “hot topic” … in many countries.

A 2011 OECD study investigated economic inequality in Argentina, Brazil, China, India, Indonesia, Russia and South Africa. It concluded that key sources of inequality in these countries include “a large, persistent informal sector (Black Markets), widespread regional divides (e.g. urban-rural), gaps in access to education, and barriers to employment and career progression for women.”[12] Here are some poignant tidbits on this subject from varied countries around the world (Wikipedia Online Encyclopedia; retrieved 09/16/2015 from: https://en.wikipedia.org/wiki/Economic_inequality):

Russia

A report by Credit Suisse in 2013 states that: Russia has the highest level of wealth inequality in the world, apart from small Caribbean nations with resident billionaires. Worldwide, there is one billionaire for every US$170 billion in household wealth; Russia has one for every US$11 billion. Worldwide, billionaires collectively account for 1–2% of total household wealth; in Russia today 110 billionaires own 35% of all wealth.[9]Western Europe

A previous blog-commentary detailed how royal charters – formal documents issued by monarch as letters patent, granting a right or power to individuals or corporate bodies – contributed to much of the Income Inequity legacy in Western European lands, and their former colonies. Among the past and present groups formed by royal charter are the British East India Company (1600), the Hudson’s Bay Company, Standard Chartered, the Peninsular and Oriental Steam Navigation Company (P&O), the British South Africa Company, and some of the former British colonies on the North American mainland, City livery companies, the Bank of England and the British Broadcasting Corporation (BBC).[2] Principals of these chartered companies became instant oligarchs; and their heirs inherited this wealth and status over the decades and centuries. In recent times however, more egalitarianism emerged, mostly because of an embrace of Neo-Socialism governmental policies and strong unions.United States

Bernie Sanders (I-VT) opined in a 2010 The Nation article that an “upper-crust of extremely wealthy families are hell-bent on destroying the democratic vision of a strong middle-class which has made the United States the envy of the world. In its place they are determined to create an oligarchy in which a small number of families control the economic and political life of our country.”[14] The top 1% in 2007 had a larger share of total income than at any time since 1928.[15] In 2011, according to PolitiFact and others, the top 400 wealthiest Americans “have more wealth than half of all Americans combined.”[16][17][18][19]Economic researchers John Schmitt and Ben Zipperer (2006) of the CEPR (Center for Economic and Policy Research) point to economic liberalism and the reduction of business regulation along with the decline of union membership as one of the causes of economic inequality. In an analysis of the effects of intensive Anglo-American liberal policies in comparison to continental European liberalism, where unions have remained strong, they concluded “The U.S. economic and social model is associated with substantial levels of social exclusion, including high levels of income inequality, high relative and absolute poverty rates, poor and unequal educational outcomes, poor health outcomes, and high rates of crime and incarceration. At the same time, the available evidence provides little support for the view that U.S.-style labor-market flexibility dramatically improves labor-market outcomes. Despite popular prejudices to the contrary, the U.S. economy consistently affords a lower level of economic mobility than all the continental European countries for which data is available.”[68]

This lesson in economic history is presented in a consideration of the book Go Lean…Caribbean. In addition to the CU, the roadmap introduces the implementation of the technocratic Caribbean Central Bank (CCB). These two entities are designed to provide better economic stewardship (governance), to ensure that the economic failures of the past, in the Caribbean and other regions, do not re-occur here in the Caribbean homeland. The book posits that we must NOT fashion ourselves as parasites of these cited countries/regions, (US, Europe or Russia) but rather pursue a status as a protégé of these powers; benefiting from their lessons-learned but molding a better society.

Consider further the US model …

The Go Lean book cites the example of the Occupy Wall Street protests of 2011, with this quotation:

Ways to Impact Wall Street – Learn from Occupy Wall Street Protest Movement – Page 200

This protest movement began on September 17, 2011, in Zuccotti Park, located in New York City’s Wall Street financial district. The main issues raised by the protests were social and economic inequality, greed, corruption and the perceived undue influence of financial service firms on the Federal government. The slogan, “We are the 99%”, referred to income inequality and wealth distribution in the U.S. between the wealthiest 1% and the rest of the population. In hindsight and as a lesson for the CU, these underlying concerns were legitimate as the 2008 Great Recession had its root causes tied to the many issues of Wall Street abuses against Main Street.Ways to Impact Student Loans – Lessons from Occupy Wall Street (OWS) – Page 160

The OWS protest movement highlighted some legitimate issues with the student loan industry. The US Federal government provides guarantees on student loans (direct and indirect), and the loans are non-dischargeable in any BK process, so private loan issuers were assured a profit. The issuers would therefore drive the industry to lend more and more to less capable students at high interest rates. As a result of the protest, the Obama Administration eliminated the indirect channel for student loan, taking the profit motive out of the process. The CU will [apply this lesson and] only direct lend.

For the most part, the people of the United States are good-natured and mean well. But there is a Shadow Influence in the US financial eco-system that undermines a lot of policies for the Greater Good. One theoretical framework of the field of Economics – neoclassical – has fully defined this. Neoclassical economics views inequalities in the distribution of income as arising from differences in value added by labor, capital and land. Within labor income distribution is due to differences in value added by different classifications of workers. In this perspective, wages and profits are determined by the marginal value added of each economic actor (worker, capitalist/business owner, landlord).[47] Thus rising inequalities are merely a reflection of the productivity gap between highly-paid professions and lower-paid professions.[48]

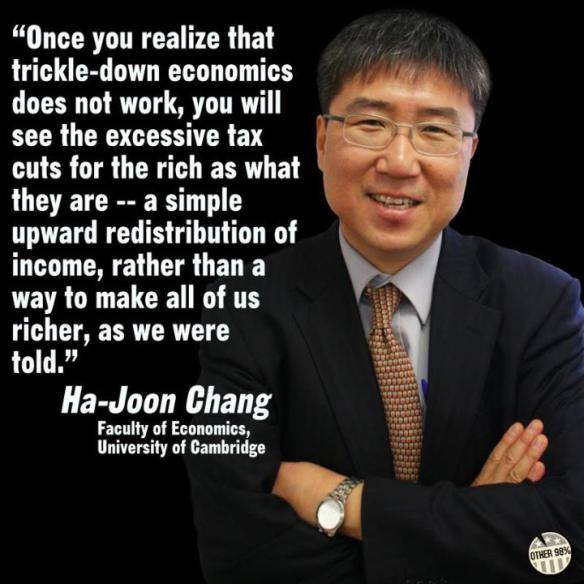

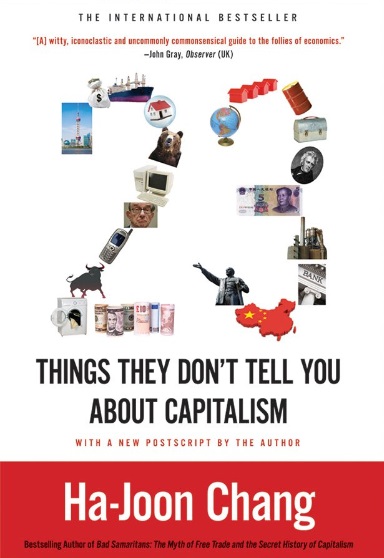

A prominent Neoclassical Economist, Cambridge University Professor Dr. Ha-Joon Chang, has emerged in recent years; he published this book 23 Things They Don’t Tell You About Capitalism. This publication addresses the width-and-breath of the subject of Income Inequality. Consider the related VIDEO and Book Reviews here:

VIDEO – “The Real News Network / TRNN” Interview with Ha-Joon Chang Part 1 – https://youtu.be/J7m9wfFnH6o

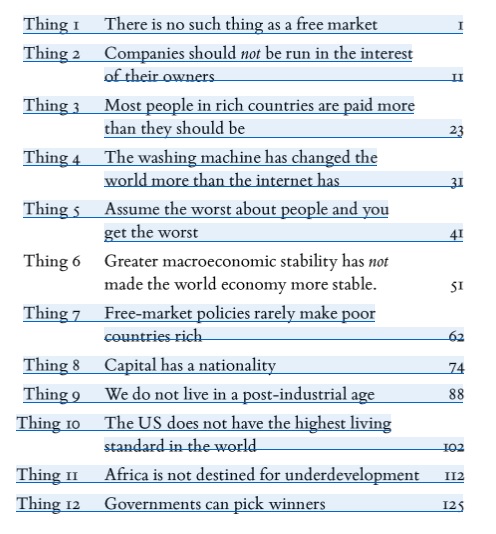

Posted April 4, 2011 – Part 1: Introducing the book 23 Things They Don’t Tell You About Capitalism with a summary of the first chapter/”Thing”: “There is no such thing as a free market”.

Part 2: https://youtu.be/4x3cS3F-SDM

Part 3: https://youtu.be/x_iLg00PuyU

Part 4: https://youtu.be/szoimtsFQEg

Part 5: https://youtu.be/RQ4Xzv9LsZs

Part 6: https://youtu.be/EhjKVo-f6Zw

Part 7: https://youtu.be/f74NPSPFTjw

Part 8: https://youtu.be/3bgcUPRnMls————-

Book Review: 23 Things They Don’t Tell You About Capitalism

Amazon Summary:

The acclaimed Ha-Joon Chang is a voice of sanity―and wit―in this lighthearted audiobook with a serious purpose: to question the assumptions behind the dogma and sheer hype that the dominant school of neoliberal economists have spun since the Age of Reagan. 23 Things They Don’t Tell You about Capitalism uses twenty-three short essays (a few great examples: “There Is No Such Thing as a Free Market,” “The Washing Machine Has Changed the World More than the Internet Has”) to equip listeners with an understanding of how global capitalism works, and doesn’t, while offering a vision of how we can shape capitalism to humane ends, instead of becoming slaves of the market.

Praise for the book 23 Things They Don’t Tell You about Capitalism:

“A lively, accessible and provocative book.” ―Sunday Times (UK)

“Chang, befitting his position as an economics professor at Cambridge University, is engagingly thoughtful and opinionated at a much lower decibel level. ‘The “truths” peddled by free-market ideologues are based on lazy assumptions and blinkered visions,’ he charges.” ―Time

Editorial Reviews

From Publishers Weekly

Chang (Bad Samaritans) takes on the “free-market ideologues,” the stentorian voices in economic thought and, in his analysis, the engineers of the recent financial catastrophe. Free market orthodoxy has inserted its tenterhooks into almost every economy in the world–over the past three decades, most countries have privatized state-owned industrial and financial firms, deregulated finance and industry, liberalized international trade and investments, and reduced income taxes and welfare payments. But these policies have unleashed bubbles and ever increasing income disparity. How can we dig ourselves out? By examining the many myths in the narrative of free-market liberalism, crucially that the name is itself a misnomer: there is nothing “free” about a market where wages are largely politically determined; that greater macroeconomic stability has not made the world economy more stable; and a more educated population itself won’t make a country richer. An advocate of big, active government and capitalism as distinct from a free market, Chang presents an enlightening précis of modern economic thought–and all the places it’s gone wrong, urging us to act in order to completely rebuild the world economy: “This will some readers uncomfortable… it is time to get uncomfortable.” (Jan.) (c)

Copyright © Reed Business Information, a division of Reed Elsevier Inc. All rights reserved. –This text refers to the Hardcover edition.Review

Leading economist [Ha-Joon Chang] has likened the nation’s acceptance of free-market capitalism to that of the brainwashed characters in the film The Matrix, unwitting pawns in a fake reality. [Chang] debunks received wisdom on everything — Rachel Shields Independent A masterful debunking of some of the myths of capitalism … Witty, iconoclastic and uncommonly commonsensical … this book will be invaluable — John Gray Observer Lively and provocative book … Read this book — David Smith Sunday Times Incisive and entertaining … scathing about the conventional wisdom’ — Robert Skidelsky New Statesman Important .. persuasive … [an] engaging case for a more cautious and caring era of globalisation — James Crabtree Financial Times Myth-busting and nicely-written … the best economists are those who look around at our man-made world and ask themselves “why?”. Chang is one — Sean O’Grady Independent –This text refers to an out of print or unavailable edition of this title.Sample Customer Review

By: William Podmore on November 2, 2010

Format: Kindle EditionHa-Joon Chang, Reader in the Political Economy of Development at Cambridge University, has written a fascinating book on capitalism’s failings. He also wrote the brilliant Bad Samaritans. Martin Wolf of the Financial Times says he is `probably the world’s most effective critic of globalisation’.

Chang takes on the free-marketers’ dogmas and proposes ideas like – there is no such thing as a free market; the washing machine has changed the world more than the internet has; we do not live in a post-industrial age; globalisation isn’t making the world richer; governments can pick winners; some rules are good for business; US (and British) CEOs are overpaid; more education does not make a country richer; and equality of opportunity, on its own, is unfair.

He notes that the USA does not have the world’s highest living standard. Norway, Luxemburg, Switzerland, Denmark, Iceland, Ireland, Sweden and the USA, in that order, had the highest incomes per head. On income per hours worked, the USA comes eighth, after Luxemburg, Norway, France, Ireland, Belgium, Austria and the Netherlands. Japan, Switzerland, Singapore, Finland and Sweden have the highest industrial output per person.

Free-market politicians, economists and media have pushed policies of de-regulation and pursuit of short-term profits, causing less growth, more inequality, more job insecurity and more frequent crises. Britain’s growth rate in income per person per year was 2.4 per cent in the 1960s-70s and 1.7 per cent 1990-2009. Rich countries grew by 3 per cent in the 1960s-70s and 1.4 per cent 1980-2009. Developing countries grew by 3 per cent in the 1960s-70s and 2.6 per cent 1980-2009. Latin America grew by 3.1 per cent in the 1960s-70s and 1.1 per cent 1980-2009, and Sub-Saharan Africa by 1.6 per cent in the 1960s-70s and 0.2 per cent 1990-2009. The world economy grew by 3.2 per cent in the 1960s-70s and 1.4 per cent 1990-2009.

So, across the world, countries did far better before Thatcher and Reagan’s `free-market revolution’. Making the rich richer made the rest of us poorer, cutting economies’ growth rates, and investment as a share of national output, in all the G7 countries.Chang shows how free trade is not the way to grow and points out that the USA was the world’s most protectionist country during its phase of ascendancy, from the 1830s to the 1940s, and that Britain was one of world’s the most protectionist countries during its rise, from the 1720s to the 1850s.

He shows how immigration controls keep First World wages up; they determine wages more than any other factor. Weakening those controls, as the EU demands, lowers wages.

He challenges the conventional wisdom that we must cut spending to cut the deficit. Instead, we need controls capital, on mergers and acquisitions, and on financial products. We need the welfare state, industrial policy, and huge investment in industry, infrastructure, worker training and R&D.

As Chang points out, “Even though financial investments can drive growth for a while, such growth cannot be sustained, as those investments have to be ultimately backed up by viable long-term investments in real sector activities, as so vividly shown by the 2008 financial crisis.”

This book is a common-sense, evidence-based approach to economic life, which we should urge all our friends and colleagues to read.

Source: http://www.amazon.com/Things-They-Dont-About-Capitalism/dp/1501266306

So how do we mitigate Income Inequality?

After presenting 23 bold statements about Things They Didn’t Tell Us About Capitalism, Professor Ha-Joon Chang, provides one more chapter, a conclusion, answering this exact question. Everyone is urged to buy his book and consume his solutions.

The book Go Lean … Caribbean, also answers a similar question: how do we mitigate Income Inequality in the Caribbean?

In summary, the Go Lean movement discourages the region from modeling the American brand of Free Market capitalism. The movement posits that America is plagued with Crony-Capitalism and institutional racism. It is therefore not the eco-system for the Caribbean to model.

On the other hand, we must give more priority to the Middle Class – as in creating 2.2 million new jobs – and less to the Rich – One Percent. (Though there is no plan to penalize their success or to forcibly redistribute any wealth).

In general, the CU will employ better strategies, tactics and implementations to impact its prime directives; identified with the following 3 statements:

- Optimization of the economic engines in order to grow the regional economy to $800 Billion & create 2.2 million new jobs.

- Establishment of a security apparatus to protect the resultant economic engines and mitigate internal and external threats.

- Improvement of Caribbean governance to support these engines.

Early in the Go Lean book, this need for careful technocratic stewardship of the regional Caribbean economy was pronounced (Declaration of Interdependence – Page 12 – 13) with these acknowledgements and statements:

xi. Whereas all men are entitled to the benefits of good governance in a free society, “new guards” must be enacted to dissuade the emergence of incompetence, corruption, nepotism and cronyism at the peril of the people’s best interest. The Federation must guarantee the executions of a social contract between government and the governed.

xii. Whereas the legacy in recent times in individual states may be that of ineffectual governance with no redress to higher authority, the accedence of this Federation will ensure accountability and escalation of the human and civil rights of the people for good governance, justice assurances, due process and the rule of law. As such, any threats of a “failed state” status for any member state must enact emergency measures on behalf of the Federation to protect the human, civil and property rights of the citizens, residents, allies, trading partners, and visitors of the affected member state and the Federation as a whole.

xxiv. Whereas a free market economy can be induced and spurred for continuous progress, the Federation must install the controls to better manage aspects of the economy: jobs, inflation, savings rate, investments and other economic principles. Thereby attracting direct foreign investment because of the stability and vibrancy of our economy.

xxv. Whereas the legacy of international democracies had been imperiled due to a global financial crisis, the structure of the Federation must allow for financial stability and assurance of the Federation’s institutions. To mandate the economic vibrancy of the region, monetary and fiscal controls and policies must be incorporated as proactive and reactive measures. These measures must address threats against the financial integrity of the Federation and of the member-states.

The Go Lean book stressed the key community ethos, strategies, tactics, implementations and advocacies necessary to regulate and manage the regional economy and mitigate Income Inequality in the Caribbean. These points are detailed in the book, as in this sample list:

| Community Ethos – Economic Principles – People Respond to Incentives | Page 21 |

| Community Ethos – Economic Principles – Economic Systems Influence Individual Choices | Page 21 |

| Community Ethos – Economic Principles – Voluntary Trade Creates Wealth | Page 21 |

| Community Ethos – Economic Principles – Consequences of Choices Lie in the Future | Page 21 |

| Community Ethos – Economic Principles – Money Multiplier | Page 23 |

| Community Ethos – Governing Principles – Lean Operations | Page 24 |

| Community Ethos – Ways to Impact the Future | Page 26 |

| Community Ethos – Ways to Impact the Greater Good | Page 37 |

| Strategy – Mission – Fortify the Stability of the Banking Institutions | Page 45 |

| Strategy – Provide Proper Oversight and Support for the Depository Institutions | Page 46 |

| Tactical – Ways to Foster a Technocracy | Page 64 |

| Tactical – Growing the Economy – Minimizing Bubbles | Page 69 |

| Tactical – Separation-of-Powers – Caribbean Central Bank | Page 73 |

| Tactical – Separation-of-Powers – Depository Institutions Regulatory Agency | Page 73 |

| Anecdote – Turning Around CARICOM – Effects of 2008 Financial Crisis | Page 92 |

| Implementation – Assemble Caribbean Central Bank as a Cooperative | Page 96 |

| Implementation – Ways to Better Manage Debt | Page 114 |

| Planning – 10 Big Ideas – Single Market / Currency Union | Page 127 |

| Planning – Ways to Improve Failed-State Indices | Page 134 |

| Planning – Lessons Learned from 2008 | Page 136 |

| Planning – Ways to Measure Progress | Page 147 |

| Anecdote – Caribbean Currencies | Page 149 |

| Advocacy – Ways to Grow the Economy | Page 151 |

| Advocacy – Ways to Create Jobs | Page 152 |

| Advocacy – Ways to Control Inflation | Page 153 |

| Advocacy – Ways to Mitigate Black Markets | Page 165 |

| Advocacy – Reforms for Banking Regulations | Page 199 |

| Advocacy – Ways to Impact Wall Street – Lessons from the “Occupy Wall Street” Protests | Page 200 |

| Advocacy – Ways to Impact Main Street | Page 201 |

| Advocacy – Battles in the War on Poverty | Page 222 |

| Advocacy – Ways to Help the Middle Class | Page 223 |

| Advocacy – Ways to Impact the One Percent | Page 224 |

| Appendix – Controlling Inflation – Technical Details | Page 318 |

The points of effective, technocratic economic stewardship of the Caribbean have been detailed in these previous blog/commentaries:

| https://goleancaribbean.com/blog/?p=6286 | Managing the ‘Invisible Hand of the Market’ |

| https://goleancaribbean.com/blog/?p=5733 | Better than America? Yes, We Can! |

| https://goleancaribbean.com/blog/?p=5597 | Economic Principle: Market Forces -vs- Collective Bargaining |

| https://goleancaribbean.com/blog/?p=3858 | ECB unveils 1 trillion Euro stimulus program |

| https://goleancaribbean.com/blog/?p=3582 | For Canadian Banks: Caribbean is a ‘Bad Bet’ |

| https://goleancaribbean.com/blog/?p=3090 | Introduction to Europe – All Grown Up |

| https://goleancaribbean.com/blog/?p=2930 | ‘Too Big To Fail’ – Caribbean Version |

| https://goleancaribbean.com/blog/?p=1731 | Role Model Warren Buffet |

| https://goleancaribbean.com/blog/?p=1309 | 5 Steps of a Bubble |

| https://goleancaribbean.com/blog/?p=1014 | All is not well in the sunny Caribbean |

| https://goleancaribbean.com/blog/?p=782 | Open the Time Capsule: The Great Recession of 2008 |

| https://goleancaribbean.com/blog/?p=353 | Book Review: ‘Wrong – Nine Economic Policy Disasters and What We Can Learn…’ |

The Go Lean book reports that the Caribbean is in crisis. There are movements on that “slippery slope”. Already the region is suffering a debilitating brain-drain estimated at 70% with some countries reporting up to 81%. This disposition is symptomatic of a Failed-State status. This roadmap attempts to reboot the Caribbean eco-systems, because we have this bad track record to contend with. The status quo must be assuaged.

It is time for change in the Caribbean! It is time to build a better society, for all: rich, poor and middle classes. Finally, the region is presented with a functional roadmap – the book Go Lean…Caribbean – where the strategies, tactics and implementations are conceivable, believable and achievable. Yes, we can make our homeland a better place to live, work and play.

Everyone in the Caribbean, the people, institutions and governments, are hereby urged to lean-in for this Go Lean roadmap. 🙂